Business Analytics: Forecasting with Trended Baseline Smoothing

This post was published 7 years ago. Download links are most likely obsolete. If that's the case, try asking the uploader to re-upload.

MP4 | Video: h264, 1280x720 | Audio: AAC, 48 KHz, 2 Ch

Genre: eLearning | Language: English + .SRT | + Exercise Files

Level: Advanced | Duration: 1h 1m | 139 MB

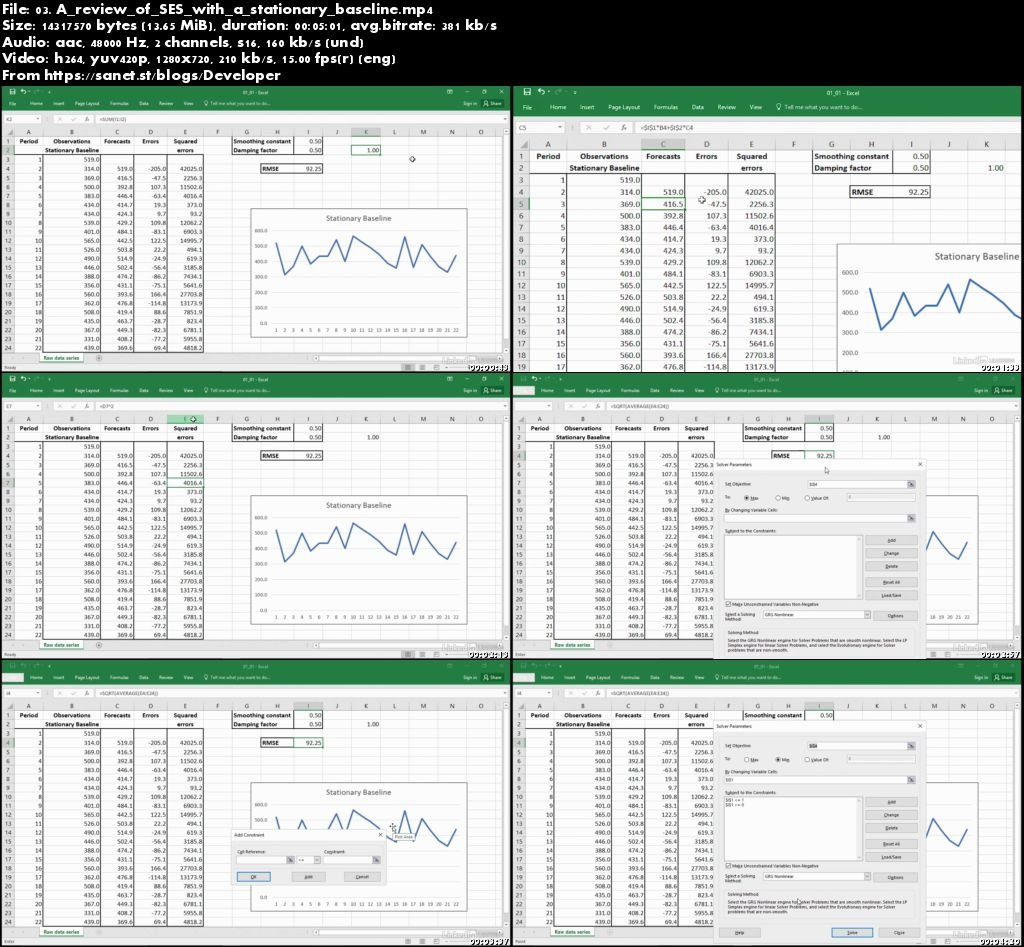

Simple exponential smoothing (SES) incorporates most of the elements used in the smoothing approach to forecasting, such as a level smoothing constant, self-correction, and the gradual weakening of the influence of older observations on new forecasts. But SES works poorly with baselines that display either trends or seasonality. The trended time series is one step up in complexity from the stationary time series analyzed by SES—its baseline trends up or down. The use of exponential smoothing with a trended baseline is often called Holt's method, and this course was designed to equip you with this technique. Here, instructor Conrad Carlberg explains how to use Holt's method to create forecasts in R that deal with trends in a baseline.

Topics include

Assembling the forecast equation for a trended baseline

Simple exponential smoothing with a stationary baseline

Using R for simple exponential smoothing

Optimizing the level and trend constants via Solver

Using R to forecast a trended series

Screenshots

Quick check before we show the links

Helps us keep automated scrapers from hammering the filehosts.